Mixed picture for Port of Antwerp-Bruges in volatile trade climate

Container traffic stabilises, bulk traffic under pressure due to international uncertainty

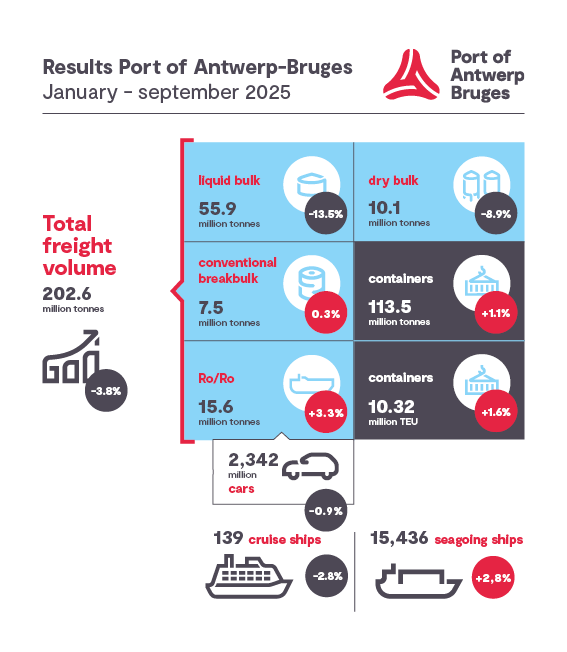

In the first nine months of 2025, Port of Antwerp-Bruges handled 202.6 million tonnes of maritime goods, a decrease of 3.8% compared with the same period last year. The throughput of general cargo, including containers, conventional general cargo and RoRo, increased by 1.3%, while dry and liquid bulk together declined by 12.8%. Following a solid first half of the year, container volumes eased from August onwards, partly as a result of the phase-out of former shipping alliances. Trade with the United States continues to be affected by ongoing uncertainty surrounding US import tariffs.

Key highlights

- Total goods transhipment falls by 3.8% in the first nine months of 2025.

- Container traffic has slowed since August, resulting in less congestion.

- Trade with the US is still growing, but American import duties are putting pressure on exports.

Slowdown in container traffic and declining congestion

After a solid first half-year, container throughput declined 2.4% in the third quarter year on year. The first nine months saw modest growth, with tonnage rising 1.1% and TEU up 1.6%.

This slowdown is linked to the normalisation of container shipping alliances, which brought an end to the temporary overlap between calls in old and new alliances. This led to a clear reduction in congestion, with quicker turnarounds and smoother traffic to the hinterland.

Port of Antwerp-Bruges’ market share in the Hamburg–Le Havre range dropped 0.7 percentage points to 29.8% in the first half of 2025, largely because of lack of terminal capacity. The bottleneck will be tackled through the ECA project (Extra Container Capacity Antwerp). Low container shipping schedule reliability and a series of strikes however continue to affect operational reliability.

Mixed trends in other segments

Conventional general cargo trade remained status quo after nine months, thanks to a recovery in steel imports, although exports remained under pressure from weaker shipments to a.o. the US and Mexico. Meanwhile, the European Commission unveiled stricter rules to curb foreign steel dumping. Liquid bulk declined 13.5%, hit by weaker petroleum derivatives exports to West Africa and persistent weakness in the European chemical sector. Volumes of biofuels and energy gases continued their growth. The decline in LNG traffic, resulting from the European ban on the transshipment of Russian gas, was partially offset by higher imports from the US. Recent announcements in the European chemicals industry underline the continued pressure on the sector.

Dry bulk (-8.9%) was primarily impacted by weaker fertiliser shipments, partly offset by increased imports from Russia and Morocco, the former ahead of the introduction of new EU duties. The RoRo segment grew by 3.3%, supported by rising imports of new cars from China – despite European import duties introduced at the end of 2024 – as well as higher volumes of trucks and used vehicles. China has now become the leading country of origin for new car imports.

Related Post

Passive Dust Control At Conveyor Transfer...

Most belt conveyors experience some spillage and dust at the transfer point, leading to safety and air quality concerns. Passive dust cont...

Hitachi Construction Machinery (Europe) NV strengthens...

Hitachi Construction Machinery (Europe) NV (HCME) has promoted Dr. Hubertus Muenster as Vice President with expanded responsibility for both...

The new generation of the SENNEBOGEN...

For more than 30 years, Entsorgungswirtschaft Soest GmbH (ESG) has been responsible for the recycling and disposal of waste from the Soest d...

Leave us a comment

logged inYou must be to post a comment.